54.5%

Throughout 2023,

we used this powerful

combination of signals to

analyze 270M devices.

.png "bck(2)")

22.4M prevented

According to Security.org, in 2023 29% of US adults were victims of an account takeover (ATO). Social media accounts were the most vulnerable accounts, representing 53% of ATOs, but online banking followed close behind at 42%.

The consequences of ATOs are severe—Security.org also found that the average financial cost of a successful ATO attack is around $12,000.

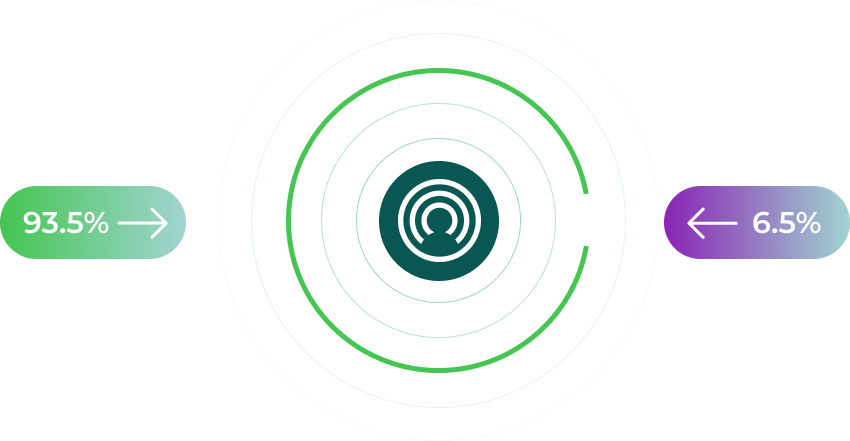

Across all 3.74B risk assessments, only 6.5% were assessed as a high risk for fraud.

.png "img__right(2)")

Device and app tampering are high indicators of risk. After all, how many regular users need to tamper with app code or hide their device IDs?

Tampering can be the first step of several fraud use cases:

Tampering Behavior

Fraudster's Goal

Delivery drivers spoofing location

Extend routes and

inflate earnings

Cloning an app to

create multiple accounts

Promo abuse

or ban evasion

Jailbreaking or rooting

Manipulate signals shared with

app alter app functionality

Fraudster spoofing location

Defeat automated fraud

prevention on logins/transactions

from new location

.png)

.png) Here are a few examples of red flags we detect that indicate app tampering:

Here are a few examples of red flags we detect that indicate app tampering:App debugging

Code injection

Risky installation

Cloned app

Frida

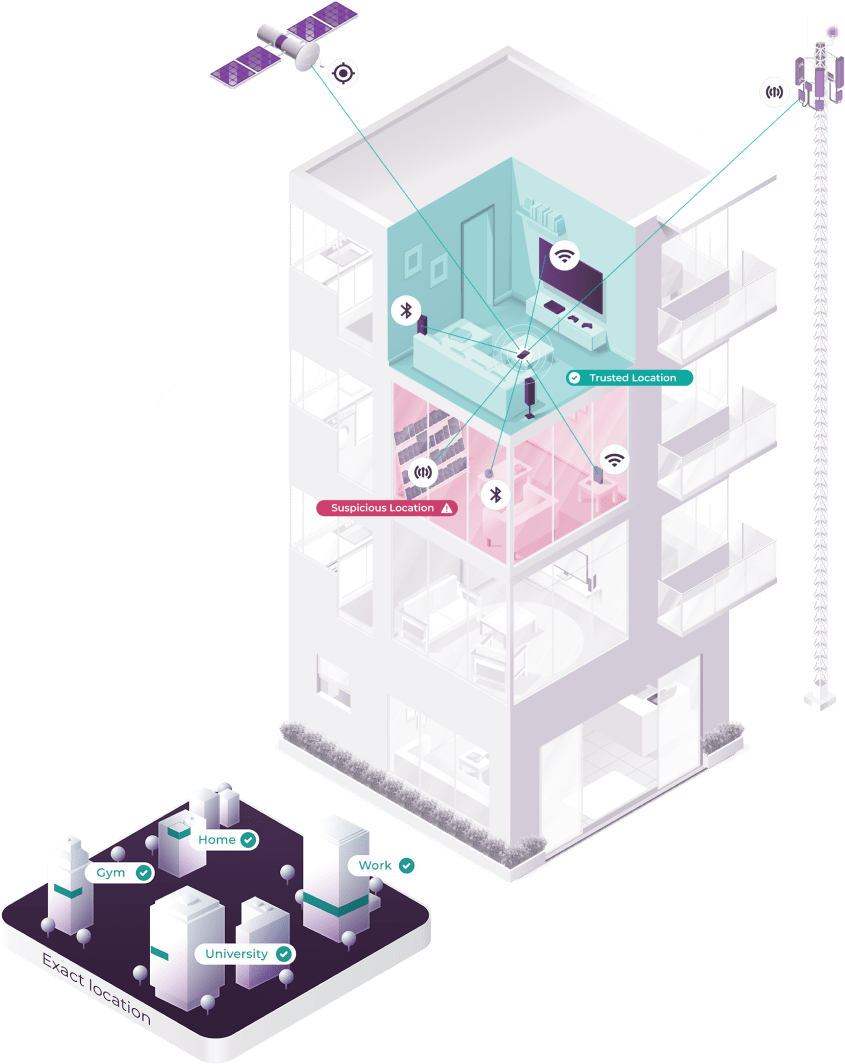

People tend to handle important account actions from a location they trust.

For example, in a 2021 analysis we found that 90% of logins on one fintech platform occurred from a trusted location.

When users suddenly start handling transactions away from Trusted Locations, that’s a higher risk indication to us that everything isn’t as it should be.

And even if a fraudster tried location spoofing a fraudulent device to make it look like it was at a Trusted Location, our solution wouldn’t be fooled. Incognia’s advanced location spoofing detection would flag that user as high risk.

.png "img__left--002(2)")